Monday, June 30, 2008

BUSINESS:

LEAF is a leading nonbasmati rice processor. It completed its expansion recently, which involved setting up a 30-mw huskbased power plant and raising rice milling capacity to 1.35 mt from 0.97 mt. It has set up wheat flour capacity of 100 tonnes per day. LEAF derives 85% of its revenue from rice processing and 15% from bran oil, de-oiled cake and branded rice. It sells 75% of its rice output to FCI at a margin of Re 1/kg. The balance is sold at higher margins in the open market. It has ventured into branded foods under the name 'Lakshmi Foods' via its subsidiary, Punjab Greenfield Resources.

The company's power plant, likely to be operational next month, will be eligible for carbon credits. Around 85% of its total power will be sold to the state government. LEAF's diversification into wheat processing is likely to generate annual profit of Rs 15 crore from the current fiscal. Wheat processing capacity will be increased to 300 tonnes per day by end FY09. LEAF has planned investments worth Rs 800 crore over the next four years. Its rice milling capacity will rise by 50%; capacities for downstream products like bran oil extraction and refining will also be expanded. Its power plant capacity will be hiked to 105 mw by '11. The branded foods segment may drive LEAF's future growth. With rising retail sales, it aims to reduce the share of FCI sales to 50% by FY10.

FINANCIALS:

Over the past three years, LEAF's sales have witnessed a 46% CAGR, while net profit has seen 89% CAGR. During the year ended March '08, it posted a 37% increase in sales to Rs 954.5 crore and 67% growth in net profit to Rs 100.9 crore. Thanks to its expansion plans, LEAF's interest cost jumped by 586%, while depreciation cost rose by 59%. Its operating profit margin improved from 13% in FY06 to 20% in FY08.

VALUATIONS:

Considering the benefits of expansion projects, power plant, carbon credits, wheat processing unit and LEAF's rising focus on retail sales, we expect the company to post a net profit of Rs 160 crore in FY09, translating into EPS of Rs 26.7. At CMP of 280, one-year forward P/E works out to 10.4, which is attractive, considering LEAF's high growth prospects.

Beta: 0.36

Institutional Holding: 40.1%

Dividend Yield: 0.3%

P/E: 12.99

M-Cap: Rs 1,681 cr

CMP: Rs 280

SOURCE: ET

Monday, June 30, 2008 0

THE DEAL:

Idea has agreed to pay Rs 77.3 per share to acquire the complete promoter stake in Spice. It will also pay noncompete fees of Rs 19 a share to the Spice promoters. This ensures that Spice will not venture into the mobile communication business for at least the next three years. The total tag for the deal comes to Rs 2,720 crore. Apart from this, Idea, along with Telekom Malaysia International (TMI), a prominent stakeholder in Spice, will make an open offer to buy 20% additional stake from existing Spice shareholders. This will cost nearly Rs 1,070 crore, though the payment procedure is not yet clear. After the merger, TMI will gain 5% stake in Idea, in exchange for its existing 39.2% stake in Spice. Later, Idea will issue preferential shares to TMI at Rs 156.96 per share to TMI, thus aggregating Rs 7,294.4 crore. Post-issue, TMI will hold close to 20% in Idea.

CAPITAL INFUSION:

Through this deal, Idea has not only acquired the business of Spice, but has also made arrangements to get funds for its future business requirements. On a net basis (after considering cash outflow to buy Spice promoters' stake, a subsequent buyback offer and cash inflow from stake sale to TMI), it will see a capital inflow of over Rs 3,500 crore. This is opportune at a time when the turmoil in global markets has made it tough for corporates to raise finances on favourable terms.

FUTURE GROWTH & CAPEX:

For Idea, the biggest benefit is Spice's existing subscriber base. The deal

boosts Idea's current subscriber base by 17% to 306 million. This also translates into an increase in market share from 9.6% to 11.2%. Moreover, Idea gets an entry into the telecom circles of Karnataka and Punjab, where it doesn't have spectrum as of now. According to experts, setting up operations in a new circle requires a breakeven period of nearly three years. Spice's operations — though not profitable at the net level due to higher depreciation and interest costs — are cash positive with operating margin of 26%. Given this, acquiring the operations of Spice makes sense. Idea has a capex plan of over Rs 10,000 crore, which reflects its aggressive strategies for future expansion. The capital to be infused by the deal will help Idea to pursue these plans. Currently, Idea has more efficient operations than Spice, given per-user capital expenditure. We expect Idea to retain its efficiency, post-merger, resulting in higher subscriber growth and improved profitability.

EQUITY DILUTION:

The deal is expected to increase Idea's equity from Rs 2,635.4 crore to Rs 3,232.6 crore. The dilution in equity and the fact that Spice's operations are still losing money on a net basis will depress Idea's EPS in the next few quarters. But this shouldn't deter long-term investors.

VALUATIONS:

At a CMP of Rs 97.5, Idea attracts the lowest per-subscriber enterprise value (EV) of Rs 10,261 among top three listed mobile operators. Its EV/ EBITDA is 11.3. This excludes impact of the merger. The deal makes Idea more expensive on these parameters as postmerger, its EV/subscriber will rise to

Rs 11,033, while EV/EBITDA will rise to 16.9. Given this, the deal appears to have come at a higher price. But we expect Spice's operations to turn around in the next 2-3 quarters. This will substantially add to Idea's overall performance in future. TMI has agreed to acquire more shares of Idea at Rs 156.96. This indicates a 61% premium over the current price and reflects the kind of growth TMI expects from this venture. Long-term investors can use the opportunity provided by the recent market fall to accumulate Idea's shares.

Rs 11,033, while EV/EBITDA will rise to 16.9. Given this, the deal appears to have come at a higher price. But we expect Spice's operations to turn around in the next 2-3 quarters. This will substantially add to Idea's overall performance in future. TMI has agreed to acquire more shares of Idea at Rs 156.96. This indicates a 61% premium over the current price and reflects the kind of growth TMI expects from this venture. Long-term investors can use the opportunity provided by the recent market fall to accumulate Idea's shares. Beta: 0.76

Institutional Holding: 10.2%

Dividend Yield: Nil

P/E: 24.7

M-Cap: Rs 25,694.8.cr

CMP: Rs 97.5

Where to shop when you have just 100 bucks. Here is the list of companies which showcase robust financials and belong to the universe of firms that trade at a price below Rs 100

Where to shop when you have just 100 bucks. Here is the list of companies which showcase robust financials and belong to the universe of firms that trade at a price below Rs 100

“Psychology is probably the most important factor in the market — and one that is least understood.”

SO BELIEVES David Dreman, the guru of contrarian investing. His statement testifies itself more often than ever in times of panic in the stock market. A slump in the market may augment manifold the impression of every bad news on the investor’s psyche. This may result in a lower risk-taking ability, while placing bets in the market.

Though at ET Intelligence Group, weclosely track the stock market and provide insights on trends and future expectations, psychology and that too, market psychology, is not our expertise. But it becomes not only an interesting exercise, but also an essential one to tap into the way investors shape their thinking during times of turbulence.

This week, ETIG presents a list of companies which have performed exceptionally well over the past three years based on a stringent set of parameters. Though this may appear to be a regular exercise from ETIG’s stable, it is unique as it takes into account only those companies whose stocks have been trading at a price below Rs 100. The reason behind drawing up such a list in the first place was to address the issue of declining risk appetite of investors who feel battered by the recent crash in the stock market. But what does it have to do with the stocks that carry a price tag of Rs 100 and below?

The general perception is that stocks of blue-chip companies, which trade at prices in three and four digits, are expensive in terms of absolute numbers. Though their ‘expensiveness’ is backed by healthy business fundamentals, investors often turn their back on these heavyweight scrips during tough times. This is because it requires a sizeable kitty to buy a good number of shares of these companies. For instance, to accumulate 100 shares of a scrip that trades at Rs 3,500, one may have to shell out Rs 3.5 lakh. In happier times, it may not be a tough call for a retail investor to go for the kill. However, during market adversities, an investor may feel apprehensive about the same bet.

In contrast, a scrip that costs, say, Rs 50 may call for a lower sum of investment and may appeal more for the same reason. This feeling of ‘buying cheap’ becomes prominent when times are bad. To help investors zero-in on the space populated by stocks that cost less than 100 bucks, ETIG carried out an exercise involving over 1,400 stocks. These were then put through a stringent criteria to select 10 stocks that fit the bill. Do read the methodology we put to use in order to get the list out.

While these companies trade at a price below Rs 100, they boast of an enviable track record. Here, we present the list of 10 companies that met our criteria.

The companies that have made it to our list are from various sectors. There are four companies from the IT sector and two from electrical machinery. The list also contains two bearings companies.

Interestingly, six out of 10 companies in our list are currently trading at a price-toearnings (P/E) multiple of less than 10. Further, the stock prices of two companies in the list have fallen more than 50% over a span of one year. The period encompasses the current fall in the market.

We ranked the companies based on their FY07 revenues. On top was Kolkata-based storage battery maker Exide Industries. At Rs 2,085.5 crore, its FY07 net sales grew by 35.6%. This is the fastest rate of growth in the past three years. Sales further grew to Rs 3,606 crore in FY08. It has a debtequity ratio of 0.52 and generates an over 20% return on capital employed (RoCE).

Berger Paints is the second company on the list. It is among the top few paint manufacturers of India. Apart from offering a range of paints, it also provides customised home painting solutions. At a 31% RoCE, the company has a low debt-equity ratio of 0.4. With a P/E multiple of 12, it is cheap when compared to the industry average of 24. However, its net profit margin is comparable at 7%.

Teledata Informatics, which currently trades at Rs 15.9, is the third biggest company in our list. It provides software solutions to utilities and education sectors and also offers network communications solutions. The company has been recording robust financials. However, its valuations have undergone a substantial decline over one year. The company, which was trading at a P/E of about seven times its trailing 12 month earnings, now trades at a P/E of about one. It needs to be mentioned that the company demerged its business late last year. Teledata’s stock has fallen by about 71% in a year, the sharpest for any company in our list. Other software companies that secured a berth in our list were Aftek, Aztecsoft and Visesh Infotecnics. Apart from these companies, bearings companies NRB Bearings and ABC Bearings also feature in our list. Each of them makes ball and roller bearings. Each of them makes ball and roller bearings. Out of the two, ABC Bearings has a higher RoCE, yet it is currently trading at a lower valuation in terms of P/E. But there is a caveat emptor. Do not mistake this list for stock recommendations. Do a little bit of your own calculations and assess your risk appetite and only then take a plunge into these stocks. As they say, past performance is no guarantee for future returns...

M E T H O D O L O G Y

AMONG 1,500 companies that were trading at a price below Rs 100, we selected companies with net sales of more than Rs 100 crore and profit after tax (PAT) of at least Rs 10 crore. We then looked for companies with robust financial performance. We started off by eliminating all those companies that had recorded less than 15% growth in net sales and PAT in any of the past three years. Further, we filtered companies on the basis of debt-to-equity ratio and return on capital employed (RoCE). While a high debt-to-equity ratio indicates that a company may not be able to generate enough cash to satisfy its debt obligations, a low leverage ratio increases a company’s potential to raise funds. Hence, we selected companies which had a debtto-equity ratio of less than 1.5. In order to carry sustainable operations, it is necessary for a company to operate at an RoCE which is well above its cost of capital. Only those companies with an RoCE of more than 15% could make it to the next stage. The final criterion was to do away with all companies whose three-year average net cash flows from operating activities was less than 50% of their reported cash profit.

Source : ETIG (Economic times)

Sunday, June 29, 2008

Cairn Energy-BUY

Scripscan:Cairn

CMP:260

Target:374

Traded in:Nse-bse

Its an interesting report from UBS and if cairn comes out with numbers as per UBS estimates-Expect huge upsides on the counter.

[Cairn india ltd news,views and analysis/Oil exploration company/turning it on/buy call given by ubs/major beneficary of high crude oil prices/upcoming results/great future prospects/going to do wonders/target price/Hidden gem/Great bet to own/what to do with cairn energy ltd?]

Upgrading to Buy on revision of UBS crude oil prices:We upgrade our rating on Cairn

Sasken Communications:Buy recommendation

Buy Aban Offshore, tgt Rs 5330: Emkay

Bull's Eye - NESTLE, GAIL, ONGC, AUROBINDO PHARMA,...

UBS raises the oil price forecasts including long-term forecast:UBS has raised the oil price forecast to US$ 113.5/120/116/135/155 per barrel in 2008/09/10/11/12 respectively primarily driven by the expectation of supplies falling short of demand substantially pulling down spare capacities. UBS has also raised its long-term oil forecast from $73/bbl to $95/bbl from 2013, on the expectations of higher cost inflation in key upstream projects and GlobalOilCo.

Raising earnings estimates for Cairn

Valuation:We change our rating to Buy and raise our target price to Rs 374. Our price target is based on our NAV estimate for Cairn

Source:UBS

Sunday, June 29, 2008 0

Saturday, June 28, 2008

Saturday, June 28, 2008 0

Biofuel technology and equipment provider Praj Industries is always loved by Stock market investors. Pune based alternative fuel major attracted legendary investors like Vinod Khosla and Rakesh Jhunjhunwala. Praj Industries is in good position to capitalise on the world search for alternative energy sources due to high crude oil prices. Praj Industries developed ground breaking Lignocellulosic technology to produce ethanol from non-crop products like Sugarcane.

1. Praj Industries started the commercialisation of Lignocellulosic technology process- Biomass magazine (July, 2008). Praj started commercialisation process 1 year earlier than analysts' expectations.

2. Praj recently got Rs 1.2 billion order for bio-ethanol equipment from UK-based Vivergo. Company set up manufacturing unit at Kandla SEZ to meet global demand.

3. Praj Industries won the Star SME award at Business Standard annual awards function.

4. Biofuel equipment agreement with Maple Energy for its South American plant.

Praj Industries Stock analysis:

CMP: 165

P/E: 19.6

1 Year high-low: 273-100.

Praj Industries target price: It is better for short term investors to stay from this scrip. Long term investors can accumulate more on further fall without hesitation.

1 year target: 220-230 (EPS will be around 10 and P/E will improve to 22). This is a conservative estimate due to current bear market conditions.

Ideal investment duration: 3-4 years.

Interesting statistic: Praj Industries gave more than 2500% returns in the last 5 years.

Sasken Communications:Buy recommendation

Buy Aban Offshore, tgt Rs 5330: Emkay

Why Praj Industries is a good long term stock?

1. Praj has 10 years experiences in Biofuels and has 9% market share in global Biofuel market. It is an undisputed leader in India.

2. Lignocellulosic technology developed by Praj will provide huge commercial opportunities.

3. Government policy of ethanol blending with petrol is another opportunity.

4. It is a zero debt company which is good in high interest rate times.

5. It is in alternative energy business which has good prospects in these high crude oil price times.

6. It is providing advance technology to firms like Tata Chemicals and Praj has more than Rs 900 crore order book from 35 countries.

7. Most of the mutual funds increased their holdings in Praj Industries in May.

8. Its global acquisitions will add revenues to the balance sheet in the next 1-2 years.

9. Analysts are expecting 25% growth in sales and 30% growth in profits. Praj may beat their expectations due to Lignocellulosic technology.

10. Sugar companies will make huge investments in Biofuel space- huge demand for Praj technology and solutions.

Negative triggers for Praj Industries:

1. Change in policies of Governments towards Biofuels due to food shortage.

2. Government interference in sugarcane prices is another concern.

Advice for technical investors: Praj Industries is currently trading just above its strong support levels. Fall to below 158 levels is a concern. This information is only for the sake of short term investors.

Choppy markets hit book values of cos

Blue Chip stocks that hit their 52-week low

Bear run pushes DLF below issue price

Verdict: If you believe in the alternate energy theory, you should buy Praj Industries. It has strong management, giant investors' support, vast experience, ability to grab upcoming opportunities; ability to develop new technologies coupled with strong growth visibility made Praj Industries a strong buy for long term investors with 24-30 months horizon. Tata Sons bought 7% stake in Praj Industries and Praj is working closely with Tata Chemicals in the Biofuel space.

Wednesday, June 25, 2008

POWERGRID CORPORATION OF INDIA (PGCIL)

BSE CODE: 532898

NSE SYMBOL: POWERGRID

Current : 105,

Target : 250 in 1 year

POWERGRID was incorporated in October, 1989 with the mission of “Establishment and Operation of Regional and National Power Grids to facilitate transfer of electric power within and across the regions with Reliability, Security and Economy, on sound commercial principles”.Transmission assets and manpower from the constituent central sector undertakings namely NTPC, NHPC, NEEPCO, NLC, etc were progressively transferred to POWERGRID. POWERGRID is engaged in Construction and Operation & Maintenance of inter-State transmission system and operation of Regional Power Grids and has been notified as the Central Transmission Utility of the country.

· PGCIL has plans to invest INR 550 bn in transmission projects for the Eleventh Plan(FY08-12). This will include increasing the inter-regional power transfer capacity to more than 37,000 MW by 2012 from 17,000 MW currently. During the nine months ending December FY08, projects of INR 52.6 bn were commissioned, including INR 19 bn in Q3FY08. The company is expected to commission projects of INR 30 bn in Q4FY08. In FY09, it is expected to spend ~INR 85 bn for investment in various transmission projects. PGCIL is expected to invest ~INR 350 bn during FY10-12E.

· This year, the company has increased its inter-regional power transfer capacity from 13,700 MW to 17,000 MW. It has added about 4,800 ckt kms, 8 new sub-stations, and around 7,200 MVA of transformation capacity.

Buy RIL on a big correction

Buy Aban Offshore, tgt Rs 5330: Emkay

· The company is expected to have net profit of INR 20,343 mn in FY09E and INR 26,022 in FY10E, after inclusion of profits from telecom and Consultancy. From the telecom business, PGCIL is expected to have profits of INR 1,297 mn and INR 2,847 mn in FY09 and FY10, respectively, including profits from leasing of fibre optic bandwidth and usage of transmission towers as mobile towers.

· PGCIL currently has an overhead optic fibre network of 20,000 km, spanning 100 cities in the country. The company has order of over INR 3,000 mn from various telecom players for leasing the optic fibre bandwidth. It also holds license for national long distance dialing (NLD) and offering services as internet service provider (ISP); the company has been generating revenues from both these segments over the past two quarters.

· PGCIL is in talks with telecom players for leasing its transmission towers as mobile towers,it is expected to lease close to 23,000 transmission towers to mobile operators in the next three years.

· Power Grid Corporation of India Ltd (PGCIL) said its revenue increased to a whopping 62 per cent to Rs 125 crore during FY08. This is the first time the Company's foray into telecom business garnered such a sizeable amount in revenues. 'The company is serving major telecom players in mobile and National Long Distance Operator (NLDO) segment and is also planning to tap customers in the entertainment and broadcasting industry.

· It is planning to spread its business overseas, reports Business Line. The company is eyeing opportunities in West Asia and the African markets, with consultancy forays in Nigeria and Dubai on the anvil. The company is in talks with Dubai Electricity and Water Supply (DEWA) to operate consultancy business. Power Grid has already received a contract for laying three transmission lines in Myanmar, while the firm has completed a pre-feasibility report on a proposed under-sea transmission between India and Sri Lanka.

· According to the Budget of 2008, PGCIL can take loan from any bank around the world on a low interest rate. As observed, 26% of expenditure of PGCIL is that of paying bank loan interest. PGCIL is in process of obtaining loans for its further expansion at a low interest rate from banks around the world.

· Power Grid Corporation of India Ltd (PGCIL) has bagged a $600 million loan from the World Bank to strengthen its electricity transmission system. Announcing the loan, which is backed by a Government of India guarantee, the Bank said in a statement that the Fourth Power System Development Project (PSDP IV) would aim to reduce transmission losses and cut the cost of energy through further investments in the utility’s systems.

· PGCIL is entering Nifty. According to shareholding pattern, only 8.4% is held by public. So within 3 months, 3% will enter in Nifty basket because of which there will be shortage of liquidity in this stock.

· Power Grid Corporation of India Limited (POWERGRID) has paid an interim dividend of Rs.176.68 Crore, for the financial year 2007-08.

'A' group stocks falling prey to Inflation, hit 52...

· Three projects of Power Grid Corporation of India Limited (POWERGRID) have bagged the prestigious National Awards for Meritorious Performance instituted by the Government of India for the year 2006-07. POWERGRID’s 132 kV Transmission System in North-Eastern region received the Gold award while Silver awards were conferred on the 220 kV and 400 kV Transmission System in Western Region and the 400 kV D/C Kahalgaon-Patna-Ballia Transmission Line.

· Power Grip Corporation of India has obtained permission to generate power from coal and gas along with transmission. It can extract gas and generate power from it by own gas block.

Share Holding Pattern (%):

Promoters : 86.4

MFs, FIs & Banks : 1.3

FIIs : 4.0

Others : 8.4

We expect Power Grid to be the best runner in future years and a strong BUY is recommended.

Wednesday, June 25, 2008 0

Monday, June 23, 2008

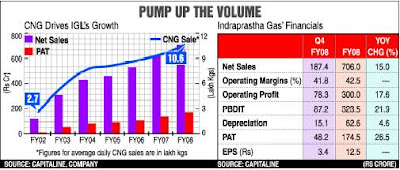

A very low beta, high dividend yield and stability in its growth outlook make Indraprastha Gas an ideal investment choice in these uncertain times INDRAPRASTHA GAS (IGL) is a Delhi-based city gas distributor promoted by GAIL, Bharat Petroleum (BPCL) and the government of Delhi together holding 50% stake. The company distributes compressed natural gas (CNG) and piped natural gas (PNG) in Delhi and nearby region. With high inflation and slowing global economic growth, the company is expected to grow steadily over the next few years, thanks to its mature business model, strong cash flows, healthy returns on capital and assured supply of natural gas.

INDRAPRASTHA GAS (IGL) is a Delhi-based city gas distributor promoted by GAIL, Bharat Petroleum (BPCL) and the government of Delhi together holding 50% stake. The company distributes compressed natural gas (CNG) and piped natural gas (PNG) in Delhi and nearby region. With high inflation and slowing global economic growth, the company is expected to grow steadily over the next few years, thanks to its mature business model, strong cash flows, healthy returns on capital and assured supply of natural gas.

BUSINESS:

Under the administered pricing mechanism, IGL gets a total allocation of 2 million metric standard cubic meters a day (mmscmd) of natural gas from GAIL, which is nearly 25% more than the company’s current gas sales.

The company derives over 90% of its revenue through the sale of CNG for automobiles, while the rest comes from PNG. During FY08, CNG sales volume increased by 12.3% to 3,862 lakh kg and PNG sales volumes increased by 17.2% to 43 million standard cubic meters (mscm) over FY07. On an overall basis the sales volumes grew 12.6% to 549 mscm during FY08.

With a number of new commercial and retail customers shifting to piped natural gas, the company has witnessed a strong cumulative annual growth of 39% over the past six years in this segment. In comparison, the sales in the CNG segment have grown at a slower rate of 25%.

GROWTH FACTORS:

After witnessing fast growth in initial years after its incorporation, the company is expected to see a steady growth in the years to come. CNG and PNG being highly cost efficient options to petrol and LPG, consumer acceptance for these

alternative fuels is growing fast. Also, expansion in adjoining regions will provide the company access to other lucrative markets. For this, the company will invest around Rs 250 crore annually over the next couple of years.

Commissioning of the Petroleum and Natural Gas Regulatory Board (PNGRB) earlier this year and its recommendations afterwards had created doubts about IGL’s future profitability. However, the marketing margins charged by the company remain out of regulatory control and hence the company is not required to change its tariff rates. This ensures the sustenance of IGL’s profit growth in future.

FINANCIALS:

IGL came out with a marginally improved performance for the

quarter ended March ’08. It earned a net profit of Rs 48.2 crore on net sales of Rs 187.4 crore. Sales were 14% higher yearon-year (y-o-y), while the net profit was up 20%. For the whole year, the company posted 26.5% growth in net profit to Rs 174.5 crore while its sales grew 15% to Rs 706 crore.

IGL has reported consistent growth in operating profit margin over the past few years. It closed FY08 with an operating margin of 42.5% against 41.2% in the previous year. However, the last quarter of FY08 witnessed a slight erosion in margin to 41.8% from 43.3% in the corresponding period in the previous year.

The company holds a healthy track record of dividends. The rate of dividend has increased consistently over last six years to reach 40% in FY 2008. At the current market price of Rs 118, this translates in a dividend yield of 3.4%.

VALUATIONS:

The price-toearnings (P/E) multiple of Indraprastha Gas at the current market price of Rs 118.7 works out to 9.5. Its peer Gujarat Gas is trading at a P/E of 9.9. The current high inflation is expected to favour the company, which offers low-cost alternatives to highcost petroleum products. Considering the growing number of CNG vehicles in the Delhi region and the fact that high prices of LPG are forcing retail consumers to shift to PNG, we expect the company to grow at 20% per annum over the next two years. A very low beta, high dividend yield and stability in its growth outlook make it an ideal investment choice in these uncertain times.

Monday, June 23, 2008 0

Low valuation multiples and an above-average dividend yield make LIC Housing Finance an interesting bet for long-term investors

The interest rates are rising due to inflationary pressure and these are testing times for housing finance companies. The recent RBI decision to hike the repo rate by 25 bps has made bankers rethink about their lending rates. HDFC, India’s largest home loan provider, has said that it will take a decision on hiking its lending rate by end-June. If it does hike the rate, it could trigger an across-the-board increase in interest rates on home loans in the industry.

However, it is important to realise that disposable income, which creates demand for home loan credit, is not expected to be hit that badly by rising inflation. Besides, young professionals are expected to continue buying homes to save taxes, as both principal and interest payments are tax deductible. Also, the demand for home loans is less elastic as compared to other loans, which provides a cushion to companies in this business in times of rising interest rates.

FINANCIALS:

The company has been on a high growth track in the past five years, as the balance sheet was expanding at a compound annual growth rate (CAGR) of more than 20%. The performance got a boost in FY08 due to widening NIMs. The impact was visible as the net profit grew by more than 40%, while the balance sheet size expanded by only 24%. This was due to a 40-basis point improvement in net interest margin, which grew to 2.85% in FY08. The company aims to maintain NIMs, as most of the loans are on a floating rate basis and it can pass on the rise in interest to the borrowers. It also expects an approximately 25% growth in business, which will translate into an equivalent growth in the bottomline, if margins remain stable. The company has a capital adequacy ratio (CAR) of 14% vis-à-vis the minimum required 12%. This provides headroom for further expansion in the loan book.

Its return on assets (RoA) was at 1.8% in FY08. This is on the lower side as compared to HDFC’s RoA of 2.4%. However, HDFC’s stock trades at more than five times its book value, while LIC Housing Finance’s stock trades at just 1.3 times its book value, which shows that the stock market has more than factored in the gap in the operational performance of the two mortgage players.

VALUATIONS:

The stock trades at a price to book value multiple of 1.3. Like LIC Housing Finance, the stocks of smaller players in the housing finance sector like Dewan Housing Finance and GIC Housing Finance also trade at low multiples. However, LIC Housing Finance is larger in scale as compared to these companies and has a better reach, which provides it better avenues of growth. The stock trades at P/E of 6.4, which seems too low considering the 25% expected growth rate in earnings in FY09. The dividend yield at current prices is 3.6%, which makes the stock an interesting bet for even conservative investors.

During times of crisis such as these, certain defensive stocks enjoy a bull run of their own, as money flows in from all directions to seek a safe refuge in them.

TROUBLE IS a strange creature — it never comes alone. Just ask any Indian investor who is currently stuck in the market and he will bear this out. With most of us having got used to an extended period of stupendous economic growth, the ongoing crisis seems to have caught virtually everyone on the wrong foot. Not only are equity investors sulking because their portfolios are melting away like an ice-candy on a hot summer afternoon, but even the risk-averse investors who trust bank deposits over everything else are feeling cheated, as double-digit inflation is eating into the real value of their savings. In fact, at current levels, the real return from a bank deposit is actually negative, given that the rate of inflation now stands higher than the deposit rate. Even the one asset, which seemed to be inflationproof — real estate — is now starting to show signs of softening. And if the performance of real estate stocks were anything to go by, then one will have to say that the worst for real estate prices is yet to come.

So, in a market such as this, the question that everyone is asking is that does one invest with an eye on the long term or just wait for the proverbial bottom to be reached? We believe that this might be an excellent time to enter the market, especially for those who have a longterm outlook. While double-digit inflation is hammering the equity market, ironically the truth is that it has made stocks a compelling investment choice by ruling out fixed-income instruments. Moreover, during times of crisis such as these, certain defensive stocks enjoy a bull run of their own, as money flows in from all directions to seek a safe refuge in them. These stocks, generally, have a strong cash flow, dividend payouts that match earnings growth, low debt or inelastic demand for the products or services that these companies make. More often than not, these companies are dominant forces in their industries to such an extent that they can become price makers and thereby insulate their bottomlines from the vagaries of inflation. They need not necessarily possess all of the above, but very often they will meet more than a couple of the above-mentioned criteria. Given our belief that in even the worst of markets, there is always hope we at Investor’s Guide decided to search for some compelling ideas that long-term investors can enter at the current levels and probably accumulate further if the market continued to slide.

For The Bravehearts

WHILE our list of storm shelters include the usual suspects from typically defensive sectors such as fast moving consumer goods and pharma, it also includes companies from capital-intensive sectors such as power and oil & gas utilities.

While it’s obvious for assetlight and cash-rich FMCG and pharma manufacturers to make it to our list, the latter are there because their financial fortune is, to a great extent, dependent on government regulations rather than market forces.

For instance, the price at which NTPC sells its power to consumers is determined by the Central Electricity Authority and not by the forces of demand/supply.

What’s more, the fact that the tariff is determined in such a manner that NTPC is virtually guaranteed a minimum 14% return on capital employed (RoCE) regardless of what the state of the economy or the inflation numbers are.

The same is the case with companies such as Tata Power, GAIL and IGL, where pricing power remains intact even in periods such as these. That said, we have decided to steer clear from large energy utility companies which are in a high investment phase and where the benefits of the same will kick in only a couple of years down the line.

Other group of stocks in our list includes agri-commodity producers such as sugar and paper makers. While the former’s fortunes are linked to the sugar cycle, the latter is a staple product with inelastic demand.

In fact, in recent times paper is one industry where realisations have shown a massive up-tick and demand outstrips supply by far.

And this mismatch is likely to continue for at least a couple of years before any fresh capacity comes into play.

Source: ETIG (Economic times)

Sunday, June 22, 2008

India's largest Engineering and Construction giant Larsen and Toubro announced very good results on thursday and company also declared 1:1 bonus issue. L&T which underperformed BSE Sensex and Nifty in the recent days will once again outperform the markets in the coming days. L&T performance in this quarter is more significant when other stocks like SIEMENS, BHEL and ABB announced below par results in this difficult quarter. These results surprised stock analysts as they are expected uninspiring performance from L&T due to losses in derivatives. Significant points:

Significant points:

1. L&T is the best managed company in India – Business Today survey.

2. Rs 600 billion order book by March 2009.

3. Larsen and Toubro will benefit from huge infrastructure investments in India and Gulf regions.

4. Future growth comes from L&T Infotech and shipping along with engineering.

5. Strong order book, good execution skills and good track record and inherent value in subsidiaries make this stock a "Must Buy".

Larsen and Toubro results analysis:  1. 55% rise in annual profit and 38% rise in Q4 net profit.

1. 55% rise in annual profit and 38% rise in Q4 net profit.

2. 41% increase in sales.

3. Operating profit rose by 54%- this is more significant.

4. Rs. 17 dividend.

5. 1:1 bonus issue.

L&T stock price analysis:

CMP: 2882

P/E: 40

EPS: 71

Face value: 2

1 Year high-low: 4,690-1,772.  L&T share target price:

L&T share target price:

It is trading at a forward P/E of 23 for FY2009 and forward P/E of 17 for FY2010. Above are estimated earnings which are routinely beaten by Larsen & Toubro.

2 year target: 120% returns.

4 year target: 300% returns. These are conservative estimates.

When will the value in L&T be unlocked? ![]() L&T will be demerged into Power, IT, Ship building and Railway units along with engineering division. Investors will get very good returns after the demerger. So go and invest for long term. You need to invest for 3-4 years to get full benefits from L&T. L&T will enter into lucrative high margin business in the coming quarters especially in the Gulf region.

L&T will be demerged into Power, IT, Ship building and Railway units along with engineering division. Investors will get very good returns after the demerger. So go and invest for long term. You need to invest for 3-4 years to get full benefits from L&T. L&T will enter into lucrative high margin business in the coming quarters especially in the Gulf region.

Verdict: L&T is a "Must have" stock in every portfolio. Like Reliance Industries, L&T also has intrinsic value. One can buy and forget about L&T for 3-4 years. If you believe in India growth story, you should buy L&T; if you don't believe in India story, you should stay away from stock markets.

Sunday, June 22, 2008 0

Friday, June 20, 2008

ScripScan:Carnation Nutra Analogue Foods

Code:531335

CMP:93

[Carnation Nutra Analogue Foods news,views and analysis/owner of nutralite brand/results/future prospects/acquired by cadilla/Analsyt buy call/cheap and attractive valuations/Solid fundamentals/great buy/Target price/What should be done with carnation nutra]

Background:Carnation Nutra is a company belonging to the Cadila Group. Cadila Group acquired the compny and thereafter came out with an open offer in the month of May 06at a price of Rs.150 per share.Cadila group currently owns 61% equity in the company.

Introduction:Carnation Nutra Analogue Foods is a manufacturer of table margarine, which sells under the brand Nutralite.Nutralite is the largest selling margarine in India with a market share of 60%.Margirine is made from refined vegetable oils and is priced comparatively cheaper to butter.Hence,making it an attractive option for general masses.Further,Nutralite can replace butter in all applications and can be used for cooking, baking, frying, and as a spread on bread, toasts, biscuits etc. Hence, there are tremendous growth prospects for the product. Carnation is targeting urban health conscious middle class segment. The company is also operating in regular diary products like butter, processed cheese & pizza cheese.As of today the margarine market is very small in India and whatever growth has achieved by the company is with zero advertising.Now the company has started aggressive marketing campaign of Nutralite including advertising on various Television Channels and distribution of samples of Nutralite free with packs of Sugar Free.

Outlook:The company has a nation-wide presence & has the second largest market share in up-markets of Maharashtra, Delhi & Gujarat after Amul.As the health awareness among Indian populace is at a never before high, the product has also shown extreme consumer interest which is only expected to increase from here.It has a strong distribution across India with several distributors.Carnation is also considering exports aimed at Middle East & African nations.

Conclusion:The market for Margirine is extremely tiny compared to butter and that will help it to register exponential growth in the years to come.The company is a debt-free entity.Carnation nutra has shown strong consitency in its topline and bottomline over the last many years.The management is aiming for a more than 80% bottomline jump in the current fiscal.The company is expected to continue with its robust growth in the coming years.Valuations at the current level looks cheap with a forward 09 P/E ratio of around 6.5.Everbody is aware of the cadila"s product "Sugar free",there is every reason cadila with its brand building experience can set the same stage for nutralite. So considering at the solid pedigree,bright prospects,huge growth,booming industry,ambitious initiatives,export potential,CARNATION NUTRA MAY JUST PROVE TO BE THE NEXT BIG THING.

Friday, June 20, 2008 0

Scrip:Pioneer Embroideries Ltd

Cmp:70

Target:150

Return expected:115%

Duration:9-12 months

[Pioneer Embroideries Ltd news,views and analysis/ Retail venture news and real estate/owner of hakoba brand/results/future prospects/Land bank/Analsyt buy call/cheap and attractive valuations/Solid fundamentals/great buy/Target price/What should be done with Pioneer Embroideries Ltd?]

Story:

Pioneer Embroideries Limited (PEL) is one of the largest players in the embroideries Et laces segment in the world.It is also India's largest manufacturer-exporter of embroideries and bobbin laces.It has got seven embroidery manufacturing units located at Mumbai, Sarigam, Naroli, Haryana, Bangalore, Navi Mumbai and Coimbatore.The company has been struggling to put on good results due to higher interst and depriciation costs but overall the turnover has been on a continuos rise.Now i like the story mostly becuase it has got a big retail and a small real estate presence.For the real estate segment the company has already signed a development agreement with Suntech Realty and it’s coming up in Borivali,Mumbai.It has also got real estates in Bangalore, in Coimbatore,Delhi and few other places as well.Plenty of you have heard the name of the retail store"Hakoba" isnt it?Its a subsidary of the company and is called Hakoba Lifestyle Limited where it owns 85% and 15% being with BCCL.The company presently has 64 outlets in 35 cities of india.The company is planning to increase the retail stores to 200 by fy09.The retail segment contributed 43crs of reveue in fy07 and the same is expected to increase at a tremendous speed going forward.At present prices of 70rs its market cap should be around 84crs.The mumbai property alone is worth 50crs,if i add up all the real estates the same would total up to 70-75crs.The company is the leader in its field with 7 manufacturing units, so the rest of the market cap gets added there.So what about the 200 hakoba stores by 09?Chow guys...You are getting them for free...64 outlets generated 43crs of revenues..how much 200 stores can?Put up the calculator and calculate coz in the scrip price of 70 it hasnt been calculated yet.

Monday, June 16, 2008

Gujarat Mineral Development (GMDC)

Report Date: June 16, 2008

CMP – Rs. 289.05

Target Price – Rs. 420/-

Mkt. Cap. - Rs. 4,595.9 crore

Recommendation : BUY

Investment Rationale

Ø GMDC has reported impressive performance for FY 2008. Net sales soared up by 66.5% to Rs 980.66 crore ledby 60.3% spurt in mining sales of Rs. 855.34 crore (Rs. 533.66 crore). Power turnover grew @ 31.8% to Rs.161.54 crore. OPM% expanded to 52.7% (47.6%) as power business turned around in Q4 FY 2008. Further aidedby 65.3% higher other income of Rs. 57.64 crore, PBT (before extraordinary items) zoomed to Rs 408.39 crore(Rs 167.75 crore). PAT shot up by 179.4% to Rs 263.93 crore (Rs 94.47 crore).

Ø GMDC has been allotted two coal mine block of 350 million mt and 250 million mt in Morga (Chattisgarh) andNaini (Orissa) to be developed over next 4 years. These mines will feed two power projects of 2,750 MW and1,750 MW with GMDC investing in 26% of their equity. However, coal supply will be at arms length and marketdetermined rates and expect coal volumes at ~15-18mn mt in the next 4-5 years. With power business turningaround in FY 2008, profitability is expected to improve further in FY 2009.

Ø GMDC is setting up 6 mtpa cement plant in joint venture with Jaiprakash Associates in Gujarat. To power thiscement plant, company would have another joint venture with Gokul Group (oilseed processing major) to set up135 mw lignite-based power plant in Surat. While GMDC will have equity in both, the cement plant will haveequity in the power plant. With captive power and cement plant, GMDC is leveraging its “coal control” capacityto turn it into components of infrastructure development, such as power, cement, etc.

Ø Thus, GMDC is set to achieve turnover of Rs 10,000 crore by FY 2012.

Valuation

At CMP (Rs 2/- paid up), share is trading at 17.4 times FY 2008 actual EPS of Rs 16.60 and at 10.3 times FY 2009expected EPS of Rs 28/-. Higher volumes and realisations should enable GMDC to grow over next few years. Thiswill be complemented by a ramp up in coal mining. Further, buoyant realisations of coal will also increaseprobability of lignite price. Hence, we recommend to “BUY” the share at CMP.

Monday, June 16, 2008 0

Friday, June 13, 2008

| Multi Bagger: C&C Constructions Ltd | |

| K.R Choksey Picks Report Dated: | |

C&C Constructions Ltd (C&C) is an infrastructure project development company providing engineering, procurement and construction (EPC) services for infrastructure projects in

Blue Chip stocks that hit their 52-week low

Bear run pushes DLF below issue price

Stocks not to Buy at this moment !!

Investment Rationale:

Robust Order Book:

C&C has a robust order book of Rs 1,668 crore (5.05x FY2007 and 3.87x TTM net sales) which has swollen by about 58.7% since FY2007. Road segment constitutes approximately 96% of the total order backlog.

Strong operating margins compared to peers:

C&C enjoys operating margins in the range 18-20%, inspite of 96% of the order backlog in road segment. The high margin is attributable to operations in areas which has geographical and political constraints. Operations from

Expertise in executing projects in inhospitable conditions:

C&C have been successful in executing projects in difficult operating terrains and adverse weather conditions which helps them in commanding higher operating margins. In addition unavailability of key resources like machinery, material and personnel along with security challenges also poses execution risk for the company.

Multibagger Stock Idea - Quintegra Solutions Ltd

FUTURA POLYESTERS LTD. - Buying strongly recommend...

Merck India Limited (MIL) - Buy Recommendation res...

Carborundum Universal : Multibagger Picks

Impressive financial performance:

C&C reported revenue CAGR of 38.6% from FY2005 to FY2007. On operating margin front also, it enjoyed industry highest margins of 29.7% in FY2006 and 23.4% in FY2007. The company plans to diversify its areas of operations into Urban

Foray into BOT space:

C&C has recently won BOT project from Kurali to Kiratpur on NH-21. We believe this project to be value accretive on the basis of IRR and is expected to contribute Rs 42 to the target price.

Valuations & Financials:

At the CMP of Rs 183.95, C&C is trading at a trailing P/E of around 8.2x and at a forward P/E of around 7.46x FY08E EPS and 5.63x FY10E EPS.

| Particulars | FY2007 | FY2008E | FY2009E |

| Net Sales | 330.47 | 573.3 | 789.5 |

| Growth (%) | 0.5605 | 0.735 | 0.377 |

| EB | 71.6 | 99.4 | 137.6 |

| Growth (%) | 0.344 | 0.388 | 0.384 |

| Net Profit | 33.2 | 46.3 | 61.4 |

| Growth (%) | 0.073 | 0.396 | 0.326 |

| EPS (Rs.) | 20.57 | 25.36 | 33.61 |

| EBIDTM(%) | 0.217 | 0.173 | 0.174 |

| NPM (%) | 0.1 | 0.081 | 0.078 |

| P/E (x) | 9.2 | 7.46 | 5.63 |

Share Holding (%) as at

| Promoters | 69.25 |

| FIIs | 9.09 |

| Mutual Funds/ Banks | 9.93 |

| Other Corp | 1.99 |

| Public and Others | 9.74 |

gem worth investing - TITAN INDUSTRIES

gem worth investing - RELIANCE PETROLEUM

gem worth investing - HDFC BANK

Friday, June 13, 2008 0